Behavioral Biases – The Hidden Forces Sabotaging Your Money Decisions

Outsmarting Yourself: 5 Common Biases That Sabotage Smart Investors

When it comes to investing, the greatest threat to your portfolio isn’t market volatility—it’s your own brain.

A behavioral bias is a mental shortcut our minds use to make decisions quickly. While these shortcuts can be helpful in daily life, they often lead us astray when it comes to complex or high-stakes situations, like investing. (Kahneman and Tversky, 1979).

Importantly, no one is immune. Even seasoned professionals with decades of experience can fall into mental traps. In fact, research shows that confidence in one's financial knowledge can increase susceptibility to bias (Pompian, 2006). That’s why self-awareness is a critical skill for investors.

Let’s explore the five most common behavioral biases in investing, along with practical solutions for avoiding them.

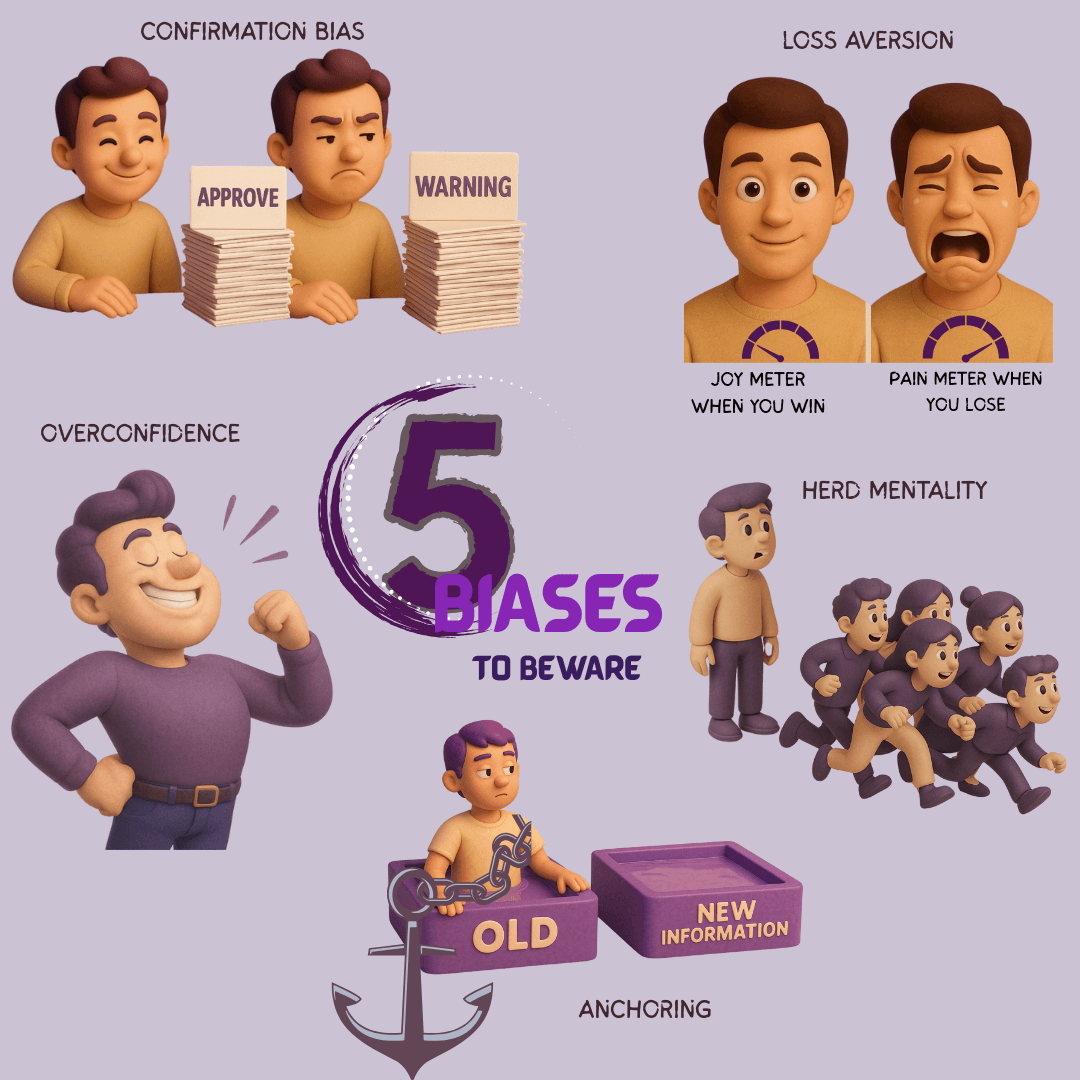

1. Confirmation Bias

The tendency to seek out or give more weight to information that confirms your existing beliefs while ignoring or undervaluing contradictory data.

Example:

You’ve heard of a new investment opportunity in a school building project that promises returns unlike any other company in the field. Because you like the return structure and it could make you a lot of money, you've already made up your mind that you want it to be true. Instead of seeking objective information that gives a realistic picture, you only look for (and rely on) positive news while discarding warning signs or any data that contradicts what you want to believe.

How to spot it: Ask yourself, “Am I avoiding information that challenges my view?”

Tool to combat it: We are VERY good at convincing ourselves that we’re being rational and objective, especially when we really want something to be true. The best way to combat this bias is with an external party, either an expert in the field or someone who can help ensure you’re not just considering information that confirms your existing beliefs.

2. Loss Aversion

Studies show that humans feel the pain of losses more intensely than the joy of equivalent gains. This leads to the second bias: Loss Aversion. It can manifest in two ways: 1) holding on to losing investments too long in hopes they’ll recover or 2) avoid risk entirely, even `good risks,` that is sensible to take.

Example 1:

You bought a stock at R100. It’s now R60, but you refuse to sell because you believe, “I haven’t lost until I sell,” ignoring the outlook that the company prospects have worsened and are unlikely to recover.

How to spot it: If you wouldn’t buy the stock today at its current price, why are you still holding it?

Example 2:

An 28 year old investor that keeps his money in the bank or in an interest bearing account due to fear of stock market movements. A young investor with ample time has greater ability to stomach market fluctuations, and being invested in higher risk assets is a sensible risk, given there is no other personal finance factors at play.

How to spot it: Is your choice based on understanding of the product / investment, or fear. If its fear, ask yourself if you would be missing out on sensible growth and wealth given its a solid investment with a good track record?

Tool to combat it: Get an expert`s objective opinion. Financial advisers are trained in behavioral biases and can help determine whether it is objectivity or your loss aversion bias in the driver's seat. (Kahneman and Tversky, 1979).

3. Herd Mentality

The tendency to follow the crowd, often driven by FOMO (fear of missing out) or the belief that so many people can’t be wrong. The problem with this bias is twofold: just because everyone is doing something doesn’t mean it’s a good decision, and following the crowd doesn’t account for how your financial situation or investment goals may differ from theirs.

Example:

Everyone is investing in cryptocurrency. You jump in, not because you understand it or even think it's a good investment, but because you don’t want to be left behind.

How to spot it: If your reason for buying starts with “everyone else is doing it,” pause. If it starts with "what if I miss out, the time to get in is now", pause.

Tool to combat it: Keep an investment journal, write down why you’re making an investment. If your reason isn’t backed by personal research and logic, rethink the move (Statman, 2014). If you do not have any information but want more information, rather contact an investment specialist. It is their job to research and understand investment instruments. Better to pay for knowledge than hop on a free ride with a mystery driver.

4. Anchoring Bias

Relying too heavily on the first number or piece of information you receive, even when it’s no longer relevant. Stay mindful of how initial information or reference points shape your outlook. In the context of investing, one consequence of anchoring is that market participants with an anchoring bias tend to hold investments that have lost value because they have anchored their value estimate to the original price rather than to current fundamentals the instrument.

Example:

You saw a stock trading at $200 last year. Now it’s $150, and you assume it’s a bargain, even though the company’s outlook has worsened. In sales, a marked-down price is often shown next to the original price to anchor you to the higher number and make the deal seem more valuable.

How to spot it: Ask yourself, “Is this decision based on outdated information or comparisons that no longer apply?” Ask yourself if the anchor is significant or simply a bias.

Tool to combat it: Use a quarterly re-evaluation checklist to assess current fundamentals rather than relying on past prices (Pompian, 2006). Fact-check everything to that you end up with credible information. This leads to a well-rounded method of getting as much information on the table as possible.

5. Overconfidence Bias

Overestimating your knowledge or intuition and believing you can outperform others.

Example:

You’ve had a few successful trades, so you start investing more aggressively, skipping research or ignoring diversification, believing you can “beat the market.” You might even feel you no longer need an adviser because your fund choices have been doing well, and you decide to fire your adviser. Easily accessible online information, or simple luck in random investments, may lead investors to believe in their own expertise more than they should.

How to spot it: If you think you’re “smarter than most investors,” that’s a cue to double-check your thinking.

Tool to combat it: Use an accountability partner, share your investment logic with someone you trust. If they can poke holes in it, you’ll gain clarity and reduce risky moves (Barberis and Thaler, 2003). A financial advisor can also assist with overconfidence bias by offering clients alternative perspectives and additional information.

It's About Awareness, Not Elimination

You can’t completely eliminate behavioural biases, they’re part of being human. But by staying aware, building systems, and asking better questions, you can reduce their influence and avoid defaulting to their instinctive pull.

Having an investment professional in your corner is especially valuable when market swings begin to trigger behavioural biases. Sometimes, the best thing an adviser can do for their client is convince them to do nothing.

If nothing has changed in your personal circumstances, then neither should your investments.

In investing, it’s not just about knowing the numbers, it’s about knowing yourself and the biases your brain will inevitably encounter.

REFERENCES:

Barberis, N. and Thaler, R., 2003. A survey of behavioral finance. In: G.M. Constantinides, M. Harris, and R. Stulz, eds. Handbook of the Economics of Finance. 1st ed. Amsterdam: Elsevier, pp.1053–1128.

Kahneman, D. and Tversky, A., 1979. Prospect theory: An analysis of decision under risk. Econometrica, 47(2), pp.263–291.

Pompian, M.M., 2006. Behavioral finance and wealth management: How to build optimal portfolios that account for investor biases. Hoboken, NJ: John Wiley & Sons.

Statman, M., 2014. Behavioral finance: Finance with normal people. Borsa Istanbul Review, 14(2), pp.65–73.

Montier, J., 2007. Behavioural investing: A practitioner's guide to applying behavioural finance. Chichester: John Wiley & Sons.